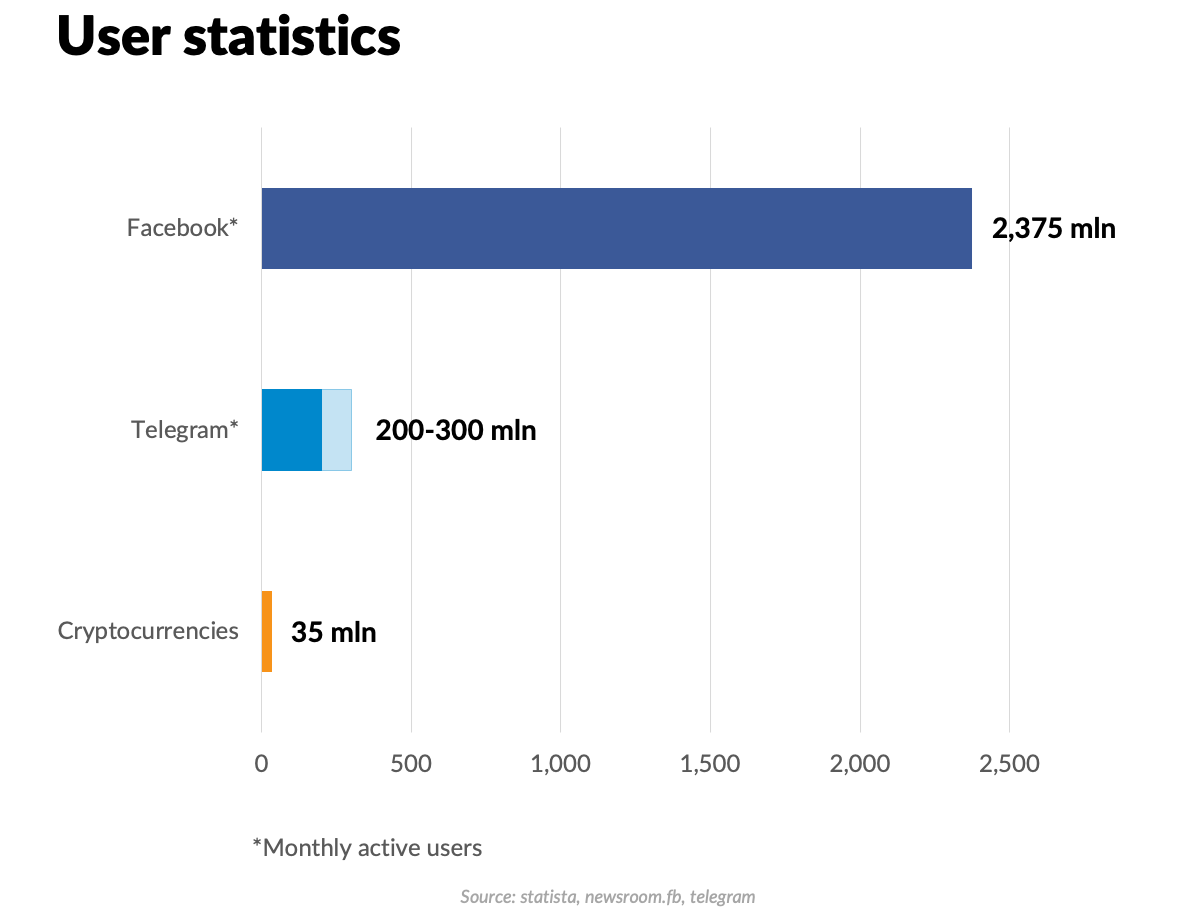

2019 has marked itself not only with the end of the crypto winter but also with time when established technology companies entered the blockchain field. Telegram is going to release its own blockchain with the goal of processing millions of transactions per second. Facebook plans to introduce Libra coin to facilitate payments for 1.7 billion unbanked but connected people.

These companies bring in not only experienced teams and massive war chests but also existing user bases and use cases. And this could be all the difference.

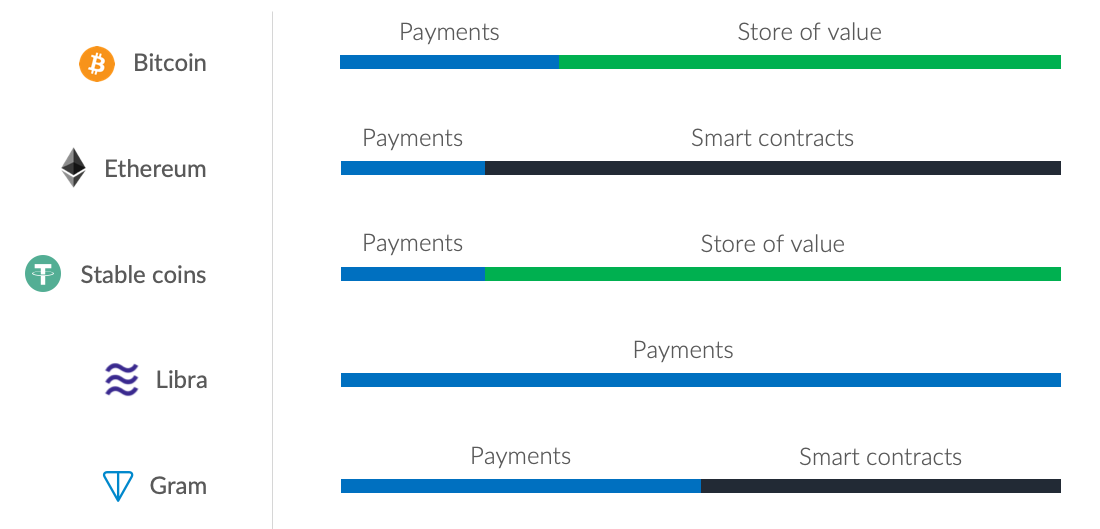

According to the economic theory, the price of an asset is driven by its intrinsic value. It turns out that major cryptocurrencies do have intrinsic value, driven by their use cases. To answer the question of whether the rise of Gram and Libra would mark the end for Bitcoin and Ethereum, we need to analyze their use cases and a brief history of the blockchain.

Bitcoin and blockchain 1.0

Despite all the hype with its price swings, Bitcoin is genuinely used as a means of payment between the parties, especially when it comes to cross-border payments.

Indeed, Bitcoin’s seven transactions per second might seem to be awfully long when it comes to paying for the pizza. But this is lightning fast for a transborder payment. This is why many websites that sell adds and freelance content writers accept bitcoin.

It’s hardly a surprise to see that Bitcoin has a meaningful adoption in the underbanked countries.

The table above also shows that people use Bitcoin as a store of value in countries with high inflation, like Venezuela. We also saw an uptick in Bitcoin trading activity in Turkey amid recent turbulence in the country and economy.

Because of the fact that Bitcoin is the oldest cryptocurrency and is decentralized, traders adopted it as a digital gold to store value in cold wallets.

It is an open question to what extent Bitcoin price is defined by speculative trading and what remains to these use cases, still if there is any fundamental value of Bitcoin it is driven by them.

Ethereum and blockchain 2.0

Ethereum opened up a new way of operating with digital assets. In fact, Ethereum created digital assets by means of ERC-20 tokens and Initial Coin Offerings.

Most of them were using smart contracts and hence accepted only ETH. Even when an ICO accepted Bitcoin and other cryptos, participants favored ETH for the speed of transactions. All this resulted in congestion of the network during highly anticipated ICOs.

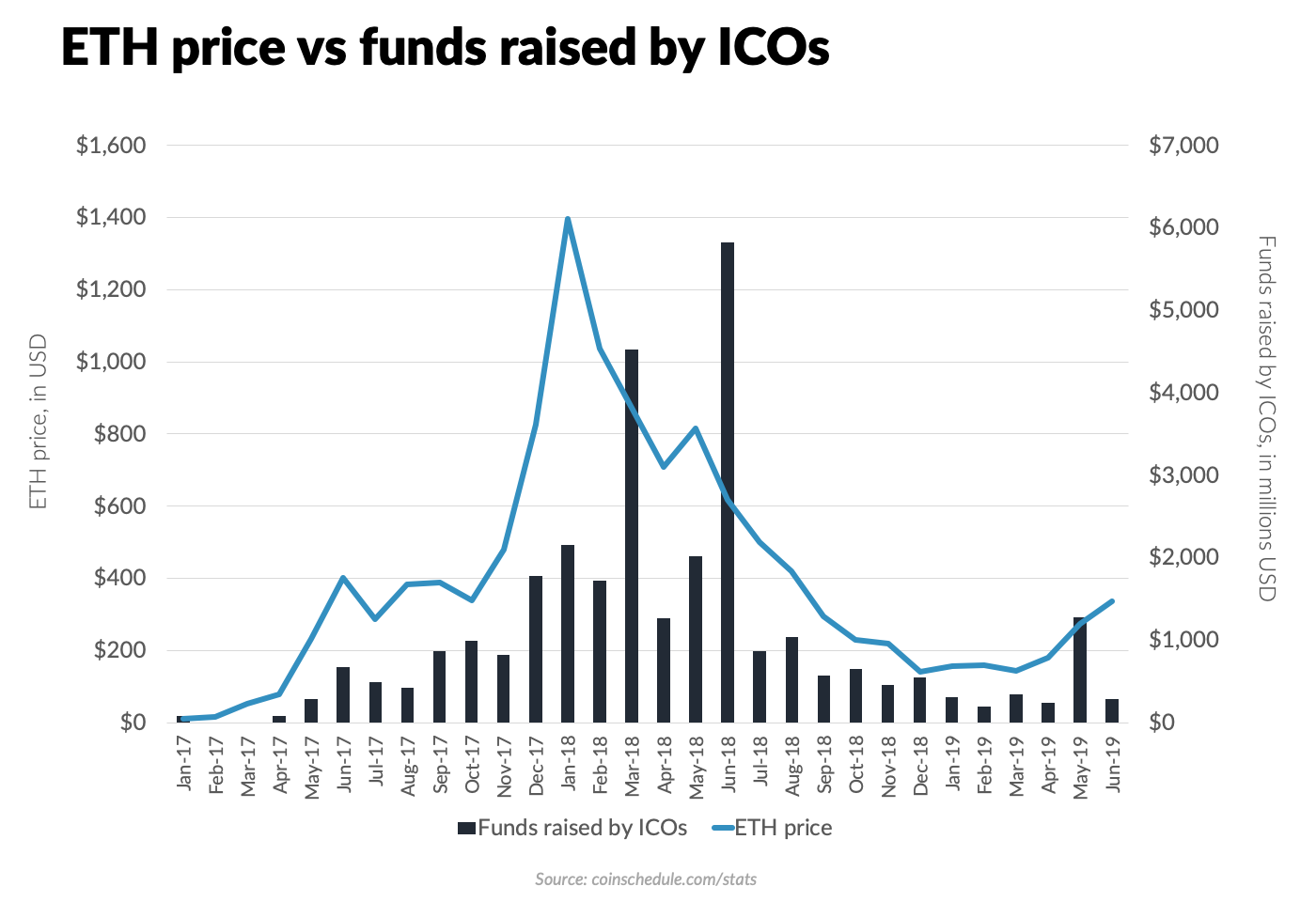

It is hardly a surprise that the ETH price skyrocketed amid the growing number of ICOs back in 2017 and fell back accordingly.

With the ICO volume decreasing, leaving the space to IEO, the use cases for Ethereum have narrowed to support ERC tokens of other projects and niche collectibles like crypto kitties, puppies, cuties and the like.

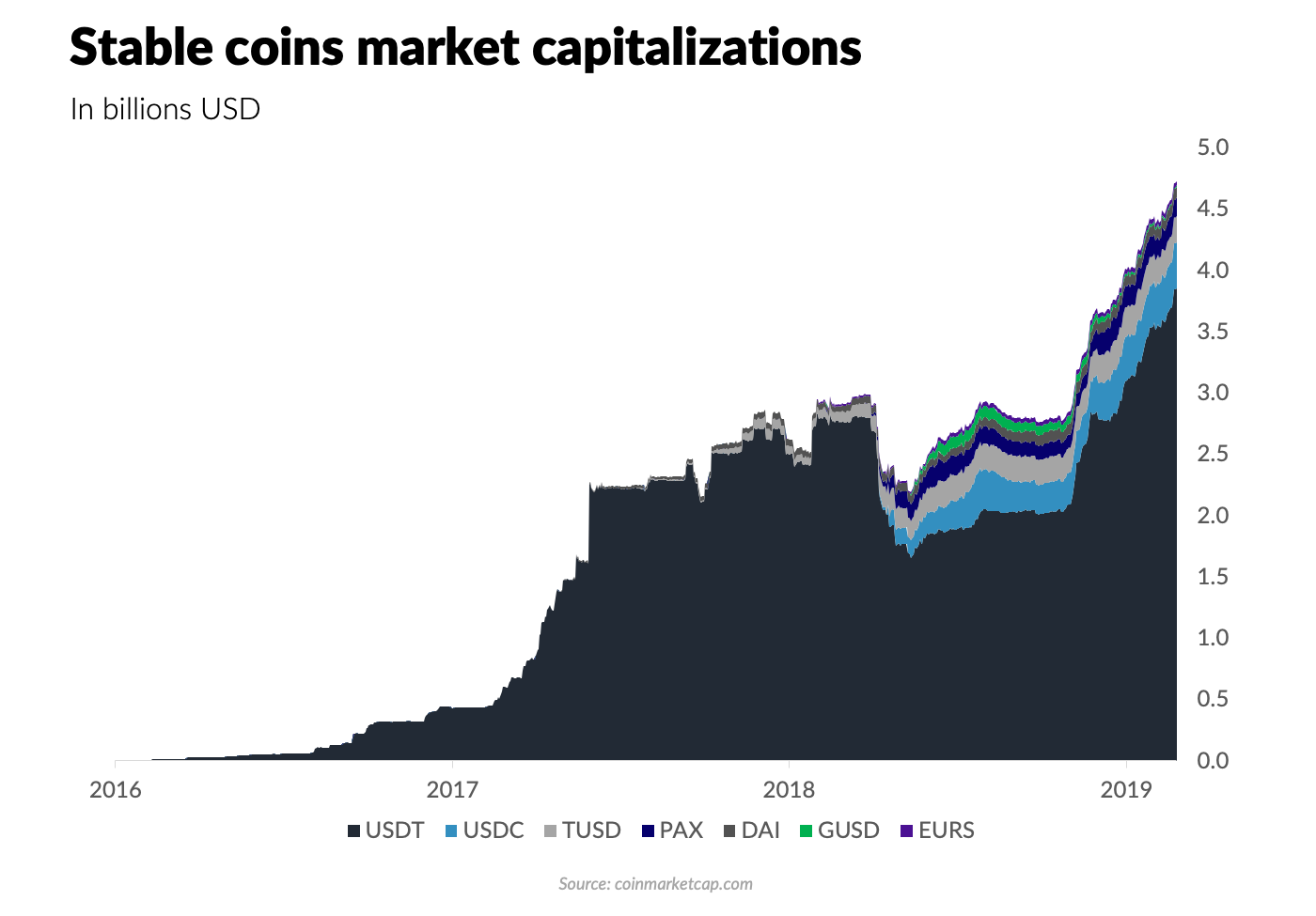

Thanks to the easiness to create and transact an ERC-20 token, Ethereum created a boost for asset-backed coins, including stable coins.

Stable coins and blockchain 2.5

Not all stable coins are Ethereum-based. For instance, controversial Tether has the majority of the tokens operating on Omni blockchain. Still, the proliferation of various stable coins is a recent development.

The use case for stable coins manifests itself in the very name. Stable coins are used as a proxy to fiat currencies and hence, the store of value. It is the closest traders could have to get into cash amid market meltdowns and projects that are willing to cash out by selling crypto assets. One could refer to the sale of round 1 Grams on Liquid exchange where only USD and USDC were accepted.

There are two major issues that limit the use cases of stable coins:

Trust;

Mass adoption.

Trust affects above all the store of value use case. Should the users believe that the stable coin is not fully asset-backed, its value shall deteriorate. This is exactly what happened to Tether in early 2017 and late 2018.

Mass adoption affects the payments use case. If it is difficult to accept payment, the transaction is unlikely to happen.

Libra and blockchain 2.6

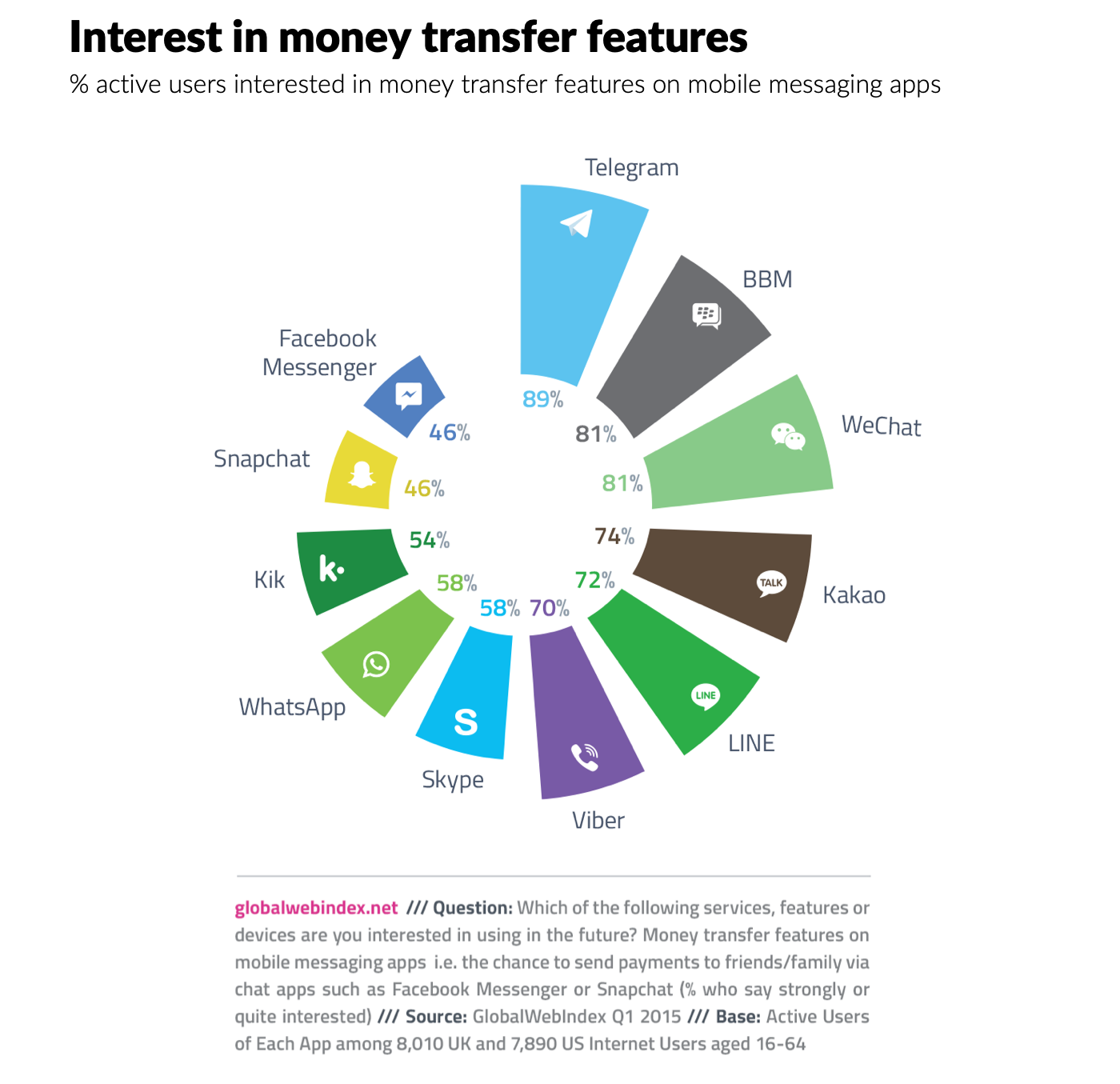

The launch of Libra by a consortium of companies led by Facebook will open a new epoch for blockchain adoption, even though it’s not actually a blockchain. Thanks to the massive user base of Facebook, WhatsApp, and Instagram, the soon-to-be-launched digital currency will have multiple use cases.

The major use cases are sending money and paying for goods and services. It’s not a surprise that the leading payment providers joined the Libra Association: Visa, MasterCard, and PayPal, to name a few.

Given the fact that Libra is going to be a stable coin, pegged to a basket of low volatile currencies, it poses an existential threat to blockchain 2.5 multiple and diverse stable coins issued by less known companies. Why should people bother using any other stable coin if one could send money directly from her Facebook account?

It will not be a surprise that the blockchain will end up with an 800-pound gorilla of Libra coin and one or two USD-pegged coin with proven reserves of fiat to serve a proxy for USD.

The open question is whether Libra poses a threat to Bitcoin. On the one hand, Libra will limit the use cases of Bitcoin. Especially that of money remittance for the underbanked. On the other, the weight of regulation and capital controls in exactly these underbanked countries tells me that Bitcoin will survive.

Libra is going to be regulated one way or another. With a centralized entity, be it Facebook or Libra Association, local regulators will send requests, subpoenas and so on. And unlike with Bitcoin regulators would have leverage since Facebook will not take the risk of being blocked by the IP.

Also, Facebook tarnished reputation after Cambridge Analytica and centralized nature of Libra will keep away those who favor decentralization. Hence even though Libra will kill the majority of existing stable coins, Bitcoin use cases will survive.

Telegram Open Network and blockchain 3.0

Telegram blockchain and its native token Gram are set to be the killer of Ethereum. TON offers the same functionality as Ethereum but on the next level, including scalability and speed of transactions. Most importantly, Telegram has approximately a 300 million user base which dwarves the audience of all cryptocurrencies combined.

Switching cost for the crypto community will be negligible as Telegram is already a default means of communication.

The image of ultra-libertarian Mr. Durov and Telegram reluctance to share user data with governments are dramatically more appealing to the crypto community when compared to Mr. Zukerberg and Facebook.

Telegram messenger has already a vibrant bot functionality. Introduction of the native blockchain for micro-payments alone is a solid use case. Expected support of smart-contracts together with fast confirmations leave no meaningful use cases for Ethereum. Most likely, Ethereum technology would continue like the current Enterprise Ethereum Alliance and serve the needs of companies with private blockchains.

Another solid use case for TON and Grams is payments from one user to another. This is the place where Grams are more likely to clash with Libra and Bitcoin.

For the former, Telegram competes for the same functionality of in-app payments, mainly in underbanked countries. All while Telegram certainly lacks the vibrant commerce functionality of Instagram and Facebook, it tries to play on the weaknesses of the competitor when it comes to the privacy of user data. For instance, in May Mr. Durov commented on the lack of security in WhatsApp. It’s yet to be seen whether the TON ecosystem would have sufficient e-commerce oriented use cases to compete with Facebook’s Libra.

As for the latter, Telegram has potential to substitute Bitcoin when it comes to Bitcoin’s value transmission use case.

Should TON be truly decentralized and Telegram successfully continue dodging IP blocking in certain countries, there are more reasons for people to adopt faster app-based transactions in Grams than stick to Bitcoin.

Surviving blockchains and their use cases

2020 is going to mark itself with the rise of new blockchains and decline of some existing ones.

Bitcoin will remain more of a digital gold and the means of payment for those who believe in hard-core decentralization, losing use cases to Libra and Gram.

Ethereum is likely to see a decline amid narrowing use cases and technical superiority of TON.

Most of the stable coins will go extinct without making it to the broad adoption mainly because of Libra becoming the trusted stable coin with use cases beyond cryptocurrency trading. For the cryptocurrency trading, we will see one or two stable coins staying in the game to be the proxy for cash.

Libra will be the currency of choice for e-commerce and money remittance for the underbanked. Most likely, we will see challenger banks entering the space to provide credit and accepting deposits in Libra. Still, the centralized nature of Libra and an open question regarding the support of smart contracts leaves plenty of room for TON.

TON is going to experience the same dynamics as Ethereum in its early days but has the better prospects than Ethereum thanks to the existing user base and infrastructure for micropayments in bots that could become governed by the smart contracts. Ultimately we will see certain competition between Libra and Gram, but this is a long shot and a topic for another article.

You can find more stories by Sergey Vasin here.

DISCLAIMER

Investment in cryptocurrencies carries a high degree of risk and volatility and is not suitable for every investor; therefore, you should not risk the capital you cannot afford to lose. Please consult an independent professional financial or legal adviser to ensure the product meets your objectives before you decide to invest. Regional restrictions and suitability checks apply.